Private Equity Update

As noted in our original JOEIS article published in November of 2020,[1] and even more so today, the orthopedic physician group sector remains one of the most active segments of the healthcare services industry for private equity strategic partnerships and investment activity. While reimbursement and staffing cost pressures, as well as higher interest rates and other macro-economic factors, will likely force private equity buyers to scrutinize the overall quality of prospective healthcare services investments more closely in 2023, we believe that the private equity investment thesis and overall sector conviction will result in increased M&A and investment activity this year, with a particular emphasis on the orthopedic sector.

Orthopedics still very much remains an attractive area of investment for private equity because the demand for orthopedic care is high, yet the supply of orthopedic surgeons in the U.S. is relatively low. This supply and demand imbalance provides for long-term sustainable growth of orthopedic services within what remains a highly fragmented clinical specialty, thus bolstering investment interest from private equity firms seeking to form strategic partnerships with best-in-class orthopedic providers. Further, data from a recent survey of orthopedic surgeons who have partnered with private equity noted that “growth and long-term success of the clinical enterprise” were the main drivers of independent orthopedic groups pursuing private equity partnerships.[2]

Private equity’s investment thesis and strong desire to partner with best-in-class orthopedic groups, combined with the ongoing need for independent orthopedic practices to pursue growth strategies that will effectuate the long-term sustainability of their clinical enterprises, will likely provide for increased private equity investment activity in the orthopedic sector.

Ongoing and Active PE Investment Activity in Orthopedic Groups

With approximately $1.2 trillion of investment capital currently being deployed within the U.S., private equity investment activity within both the physician practice management (PPM) sector broadly, as well as within the orthopedic sector specifically, remained resilient through the majority of 2021-2022.[3]

The continued pace of this activity is likely driven by several factors, including:

-

the growing reimbursement, financial and competitive challenges facing independent practicing physicians, and their recognition that being part of a larger organization can be more effective in achieving successful clinical operations;

-

a desire to “jump on the bandwagon”, as they see more of their physician peers in highly respected orthopedic groups entering major private equity partnership transactions; and

-

the benefit of “monetizing” the value of the orthopedic practices they built over the years at tax advantaged rates and taking “chips” off the table to hedge against future uncertainties and potential de-valuation of their clinical practices.

Private equity investors will likely consider several factors when evaluating provider enterprises and determining whether they are an attractive investment platform, including (for example): group size (number of physicians and mid-level practitioners), number of locations and geographic breadth, reputation in the local market, experience with value-based care, management team, and very importantly, the type and extent of ancillary clinical services the practice has and/or could have in place (such as imaging, ASCs, PT, DME, urgent care, etc.). Investors are attracted to orthopedic groups with a demonstrable history of success and have a shared vision for continued growth on either a regional and/or national basis.

The continued growth of orthopedic group partnership activity with private equity platforms is demonstrated in the below chart, which depicts 14 of the private equity sponsored orthopedic practice platforms (8 of which commenced in the last 2 years), as well as 70 orthopedic groups across the country that partnered with these platforms.

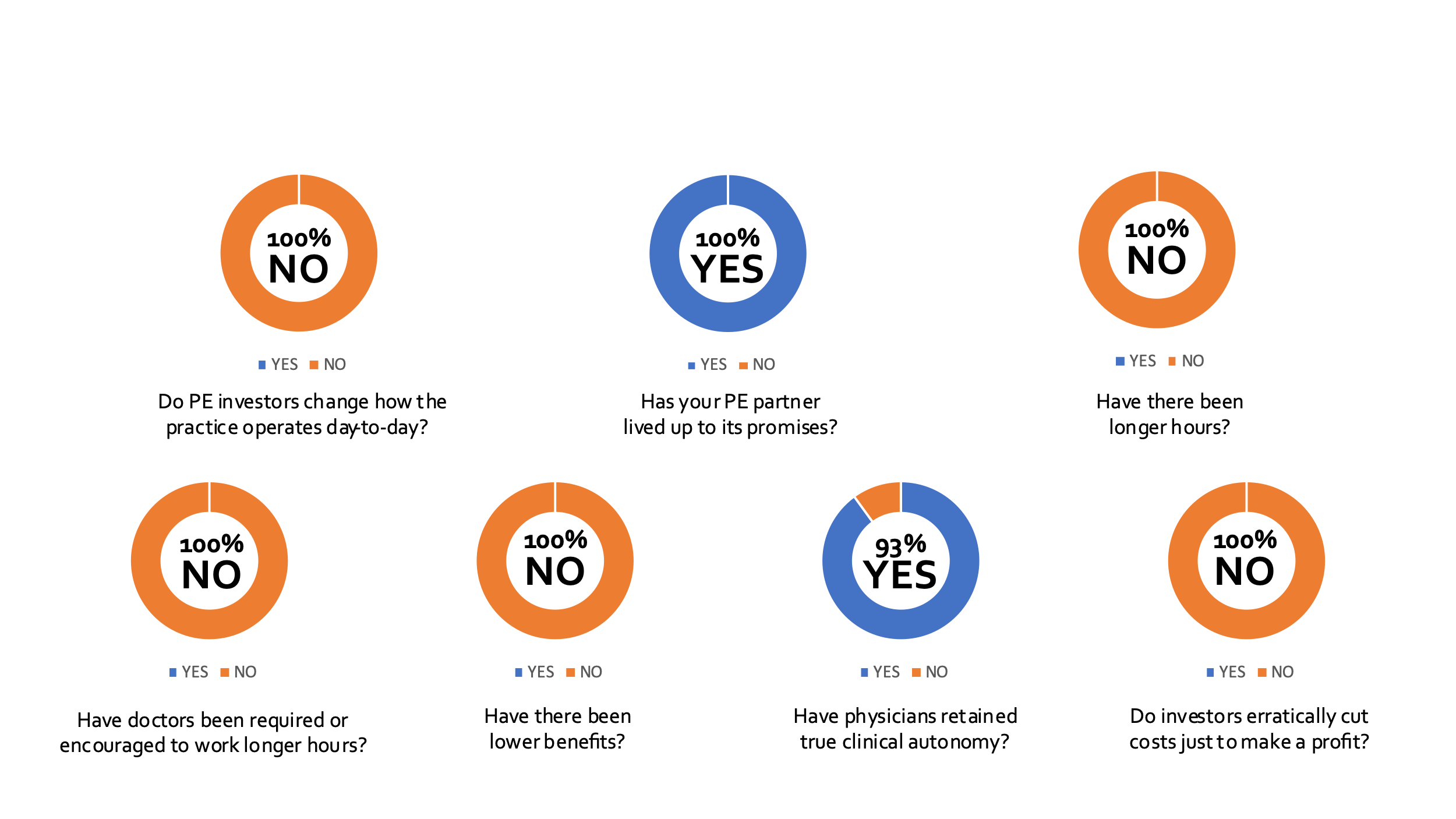

“Life After Closing” – From Orthopedic Surgeons Who Partnered with Private Equity Platforms

Vector Medical Group conducted an anonymous survey of orthopedic surgeons who entered into partnership transactions with 10 different orthopedic platforms regarding their “life after closing” of the deal.[4] The results of the survey reflect different perspectives, but there is a common theme – not much changed in their day-to-day practice of medicine since the closing.

Over 85% of responding surgeons said that their practice has been “As Expected” or “Better than Expected”, and overwhelmingly were pleased that experienced business executives were now focusing on the practice’s business operations. They also appreciated the fact that having these savvy executives resulted in the group’s “varied personalities and internal politics among physicians” being taken out of the decision-making process with respect to back-office business and operational issues. While some respondents lamented not being in control of “back office” functions and not being able to make “snap” business decisions, they also appreciated the assistance provided by platform executives on various staffing and related logistical issues.

The survey responses in the chart below largely debunk some common myths about private equity investors.

Private Equity Demand for Orthopedic Groups to Remain Strong in 2023

We believe that continued private equity investment in orthopedic groups will be further supported by growth in the number of private equity firms seeking to invest capital within this clinical specialty, followed by growth via bolt-ons of smaller groups. The demand for orthopedic treatments and procedures is continuing to increase nationwide, with both inpatient and outpatient surgeries generating $110 billion in revenue annually.[5] At the same time, many physicians are experiencing increased financial pressures in the current, rapidly changing healthcare services environment.

A partnership with a private equity investor or an existing private equity-backed platform can be an appealing option for orthopedic groups, but physicians must also understand the overall goal and objectives of private equity. While the medical, clinical, and patient care aspects of the practice will remain within the sphere of influence of the physicians in a private equity partnership – which can be confirmed via express contractual provisions – physicians will have very little influence on the business aspects of the practice. Business-related initiatives – such as the streamlining of administrative tasks, pursuit of economies of scale for purchasing, onboarding of new vendors, and installing new administrative leadership teams within the practice – are all examples of areas in which the private equity investor will lead decision-making.

The top four factors orthopedic groups should consider when contemplating a private equity partnership include:

-

Most importantly, the overall cultural fit, management team personality, common vision, healthcare-specific investment track record, and orthopedic sector expertise of the potential private equity partner organization.

-

The desire to increase the practice’s operational performance and strategic initiatives in response to both (a) ongoing changes in reimbursement and regulatory programs, and (b) increasing competition from hospitals and other large and growing healthcare organizations (e.g., OptumCare, CVS, Walgreens, Amazon, etc.).

-

The need for working capital to invest and support practice infrastructure and growth (including the addition of more physicians, office locations, ASC’s, ancillary services, EMR, virtual care, etc.); and

-

The importance of “monetizing” the value of historical physician ownership (tax-efficiently) in light of increasing competition and future risks and uncertainties.

Conclusion

A private equity partnership is not right for every orthopedic group, but before making any decisions you should become fully informed by thoroughly exploring the pros and cons of different strategic options based on the circumstances and characteristics of your group and its local market dynamics. For orthopedic groups facing one or more of the 4 key factors noted above, private equity may be an increasingly attractive option in 2023 and beyond. Other groups may decide to “stay the course” and continue practicing independently, or enter into some other strategic partnership.

Important Note: If you would like to learn more about private equity and other strategic transactions for orthopedic groups, the authors are also moderating sessions at a full day educational conference on this topic (including 10 physician speakers, and other industry experts), which is complimentary for independent physicians and leaders of independent medical groups. The conference is on March 9, 2023 in Las Vegas at the Venetian Hotel. Registration is limited based on room size. Information about this conference and registering is at: https://e-coms.ebglaw.com/19/1078/landing-pages/conference-agenda(speakers).asp

About the Authors

Gary W. Herschman, Member & Chair of Healthcare Transactions Practice, Epstein, Becker & Green, P.C.

Gary W. Herschman is a member of Epstein, Becker & Green, P.C.'s Health Care and Life Sciences practice, and serves on the firm’s Board of Directors in addition to its National Health Care and Life Sciences Steering Committee. Gary is a healthcare attorney who focuses on mergers and acquisitions and other strategic transactions. This primarily includes advising physician groups and ASCs across the country (including dozens of orthopedic groups, and many other specialty practices) on private equity partnerships, and other strategic transactions including consolidations, mergers, joint ventures, and affiliations. Gary also advises healthcare clients on regulatory compliance issues (both federal and state), which are important in connection with any transaction. (Email: gherschman@ebglaw.com)

Dana Jacoby, Chief Executive Officer

Vector Medical Group, LLC

Dana Jacoby is recognized as a difference maker and trusted advisor to health system executives, medical practices, vendors, and other stakeholders in optimizing patient care while also elevating financial and operational performance. Dana’s passion for operational excellence has driven a distinguished record of achievement at the intersection of market data, measurement and analytics, strategy design and implementation, and technology innovation. She is a published author and engages audiences as a keynote speaker, educator, and subject matter expert at medical forums, summits, and conferences. Dana has played a pivotal role in leading transformation throughout the highly regulated and value-centric health care industry. (Email: djacoby@vectormedicalgroup.com)

Hector M. Torres, Managing Director, Healthcare Investment Banking

DC Advisory

Hector M. Torres is a Managing Director within the global Healthcare Investment Banking practice of DC Advisory, a leading global investment banking and financial advisory services firm. With over 16 years of experience providing investment banking and financial advisory services to healthcare organizations nationwide, he has completed M&A transactions and financial advisory engagements with cumulative value in excess of $4.8 billion. His clients include large physician practices and groups, national and multi-regional health systems, academic medical centers, health insurers, non-acute care providers, medical device companies and capital providers to healthcare entities. (Email: Hector.Torres@dcadvisory.com)

The 2020 article, JOEIS’s most downloaded (over 10,000), has more extensive details regarding the structure and benefits of private equity transactions with orthopedic groups, and can be accessed at: https://journaloei.scholasticahq.com/article/17721-private-equity-partnerships-in-orthopedic-groups-current-state-and-key-considerations. Such article was updated in early 2022 at: https://journaloei.scholasticahq.com/post/1336

Source: Vector Medical Group independent anonymous online survey completed in January 2023 (using SurveyMonkey), as well as several individual interviews and accounts.

Source: Credit Suisse U.S. Asset Management research, December 2022.

See footnote 2 with more details on anonymous survey, as well as interviews.

Source: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7388821/.