INTRODUCTION

The cost-effectiveness across all aspects of surgical procedures is being closely scrutinized in the current value-based healthcare environment and commonly includes the assessment of operating room (OR) efficiency measured in time reduction against overall OR unit cost versus patient outcome (Cichos, et al 2019; McLawhorn, et al. 2015; Mhlaba, et al. 2014; Stockert, et al. 2014). Especially in primary total hip arthroplasty (THA) and total knee arthroplasty (TKA) procedures, these “marginal gain” aggregates are measured for procedures, surgeon technical skills, and support staff that are usually already highly optimized. Palsis, et al, investigated the costs for the entire episode of primary hip and knee arthroplasty using a time-driven activity-based costing (TDABC) methodology versus traditional accounting methods (Palsis et al. 2018). The breakdown of the entire surgeon-patient episode (initial clinic, through surgery and follow-up) was defined, and total costs assigned to each step. The continuum across the surgeon-patient episodes revealed the effects of specific steps in which various burdens could be identified, marginal gains strategies defined, applied, and measured.

Independent of the surgery type, instrument tray optimization has become a focus of cost-reduction strategies for hospitals, and ambulatory surgery centers (ASC) (Cichos, et al 2019; McLawhorn, et al. 2015; Mhlaba, et al. 2014; Stockert, et al. 2014). It has been reported that the total cost to process a single instrument is approximately $0.51 and may increase based on complexity of the instrument / specialty (Mhlaba, et al. 2014). In a single site, observational study, Stockert, et al, reported that across four surgical specialties, less than 20% of the total instruments opened are actually used during the procedure (Stockert, et al. 2014). The authors recommend that strategically assessing and re-allocating tray composition has immediate effects on various cost centers such as central processing labor and operating room instrument management.

The purpose of this study was to introduce an intra-operative instrument tray reduction strategy for primary total knee arthroplasty (TKA), and to report on the feasibility and influence of the instrument tray reduction implementation on related facility cost burden reductions.

MATERIALS / METHODS

A prospective, continuous series of 34 primary TKAs in 34 patients was performed by the senior author (CMH) within a single ASC facility. All patients were admitted, primary TKA procedures performed, and patients discharged the same day. For this study, internal IRB approval was granted, and all de-identified patient demographics and follow-up through 90 days and again at 1- and 2-years including unscheduled office / hospital visits were recorded and reviewed. Patient co-morbidities were tallied to show that this consecutive series was not selective and included all-comers.

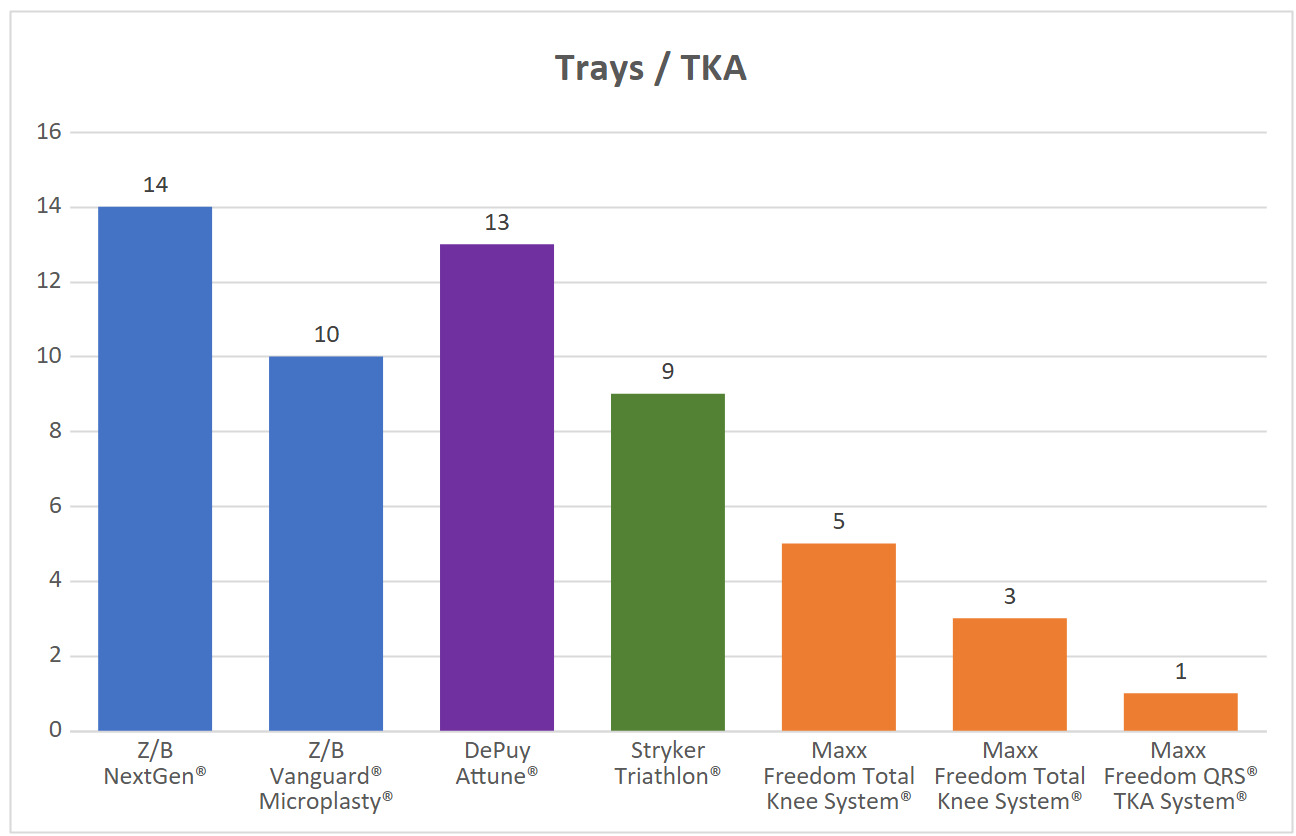

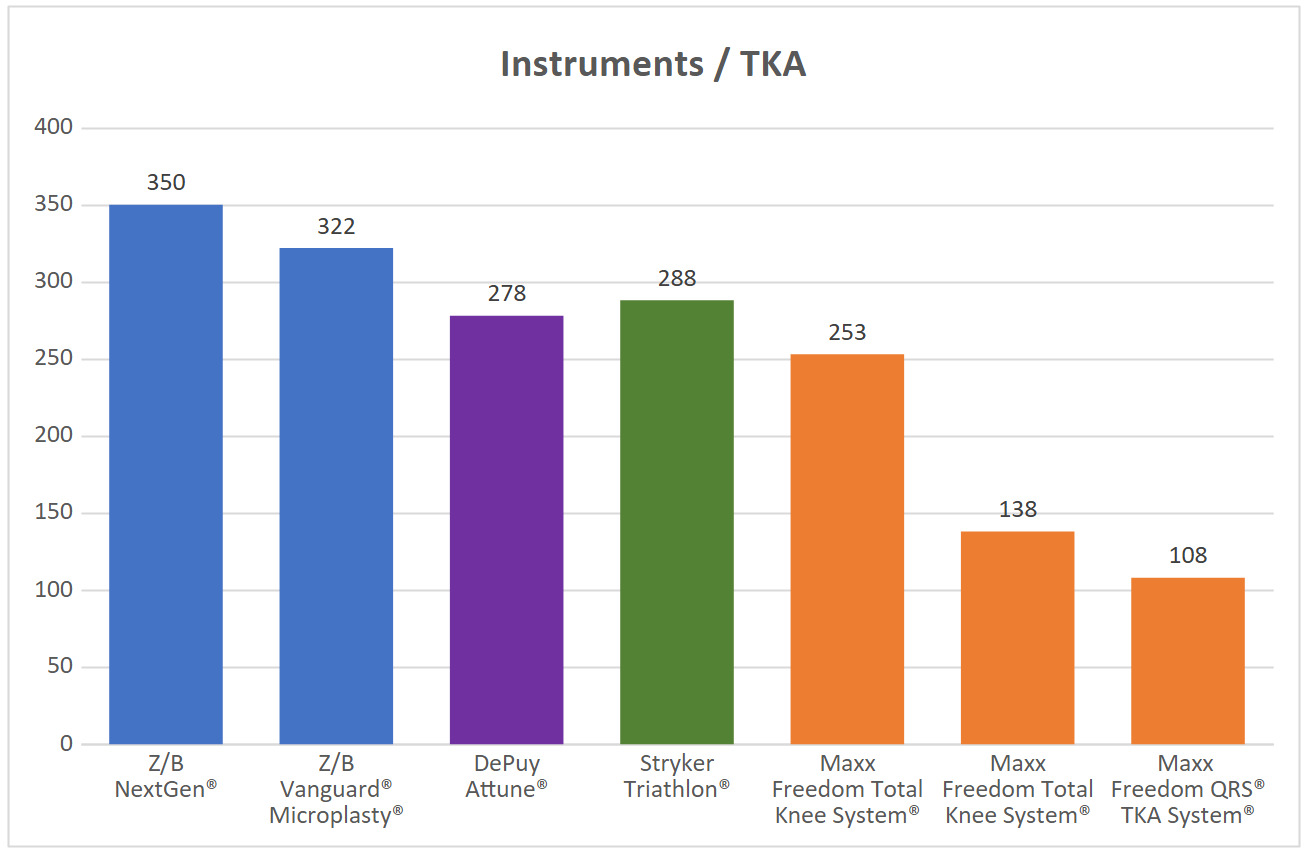

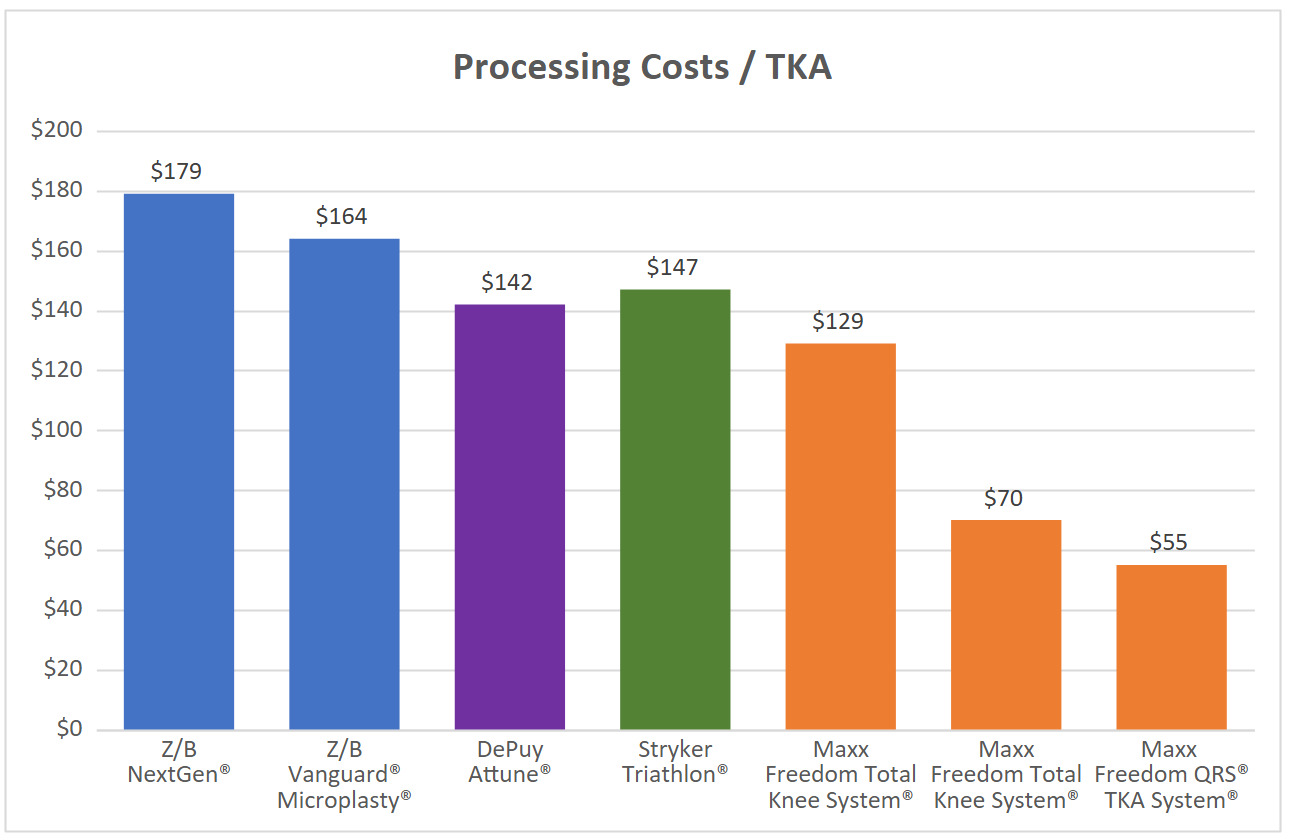

The senior author (CHH) implemented the Freedom® Quick Recovery Solutions (QRS®) Quick Tray TKA system (Maxx Orthopedics, King of Prussia, PA). This system utilized digital radiograph assessment with an automated templating system to determine component sizing, ± one size to minimize the number of component trials included and implantable product inventory. The single tray strategy also included the surgeon’s preferred / formulary of instruments related to the primary TKA system. The differences in TKA instrument tray configurations used were reviewed and assessed using the processing cost estimate of $0.51 per instrument. In addition, common TKA-specific trays and instrument counts were also assessed for processing cost comparisons. The four common TKA systems included 9 to 14 trays, and 278 to 350 TKA specific instruments (Table 2, Figures 1,2, 3A-C). Descriptive statistics were applied to this patient cohort and adverse events / unscheduled visits were assessed.

RESULTS

Of the 34 patients studied, there were 20 (59%) females and 14 (41%) males with an average age at surgery of 64.3 ±7.5 years (range: 35.4 – 75.5 years) (Table 1). All patients were clinically and radiographically followed through two-years post-operatively without loss to follow-up. The average patient BMI was 31.9 ±5.2 (range: 22.1 – 41.1) and presented pre-operatively with an average of 2.4 significant co-morbidities (range: 0 – 6). These demographics clearly indicates that this study included all patients with no pre-selection.

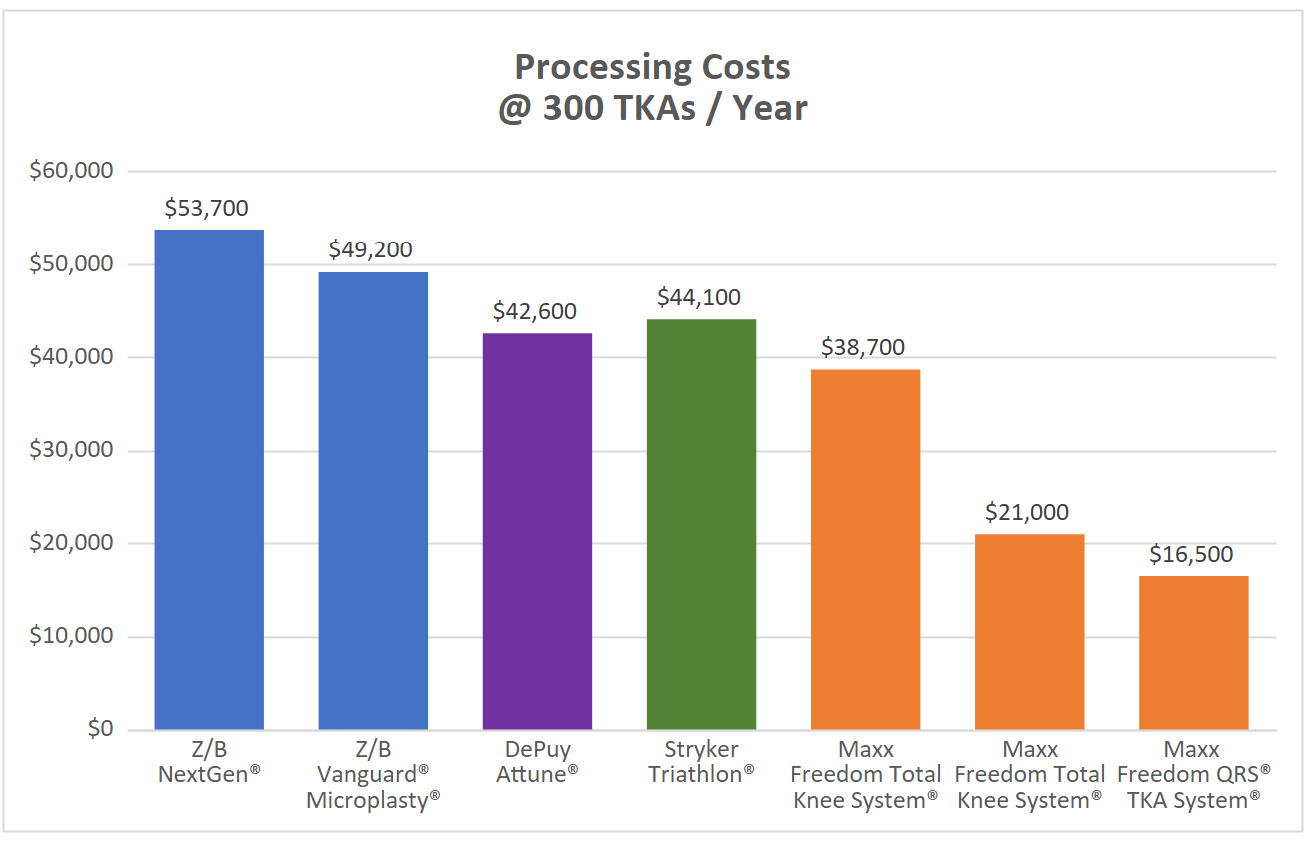

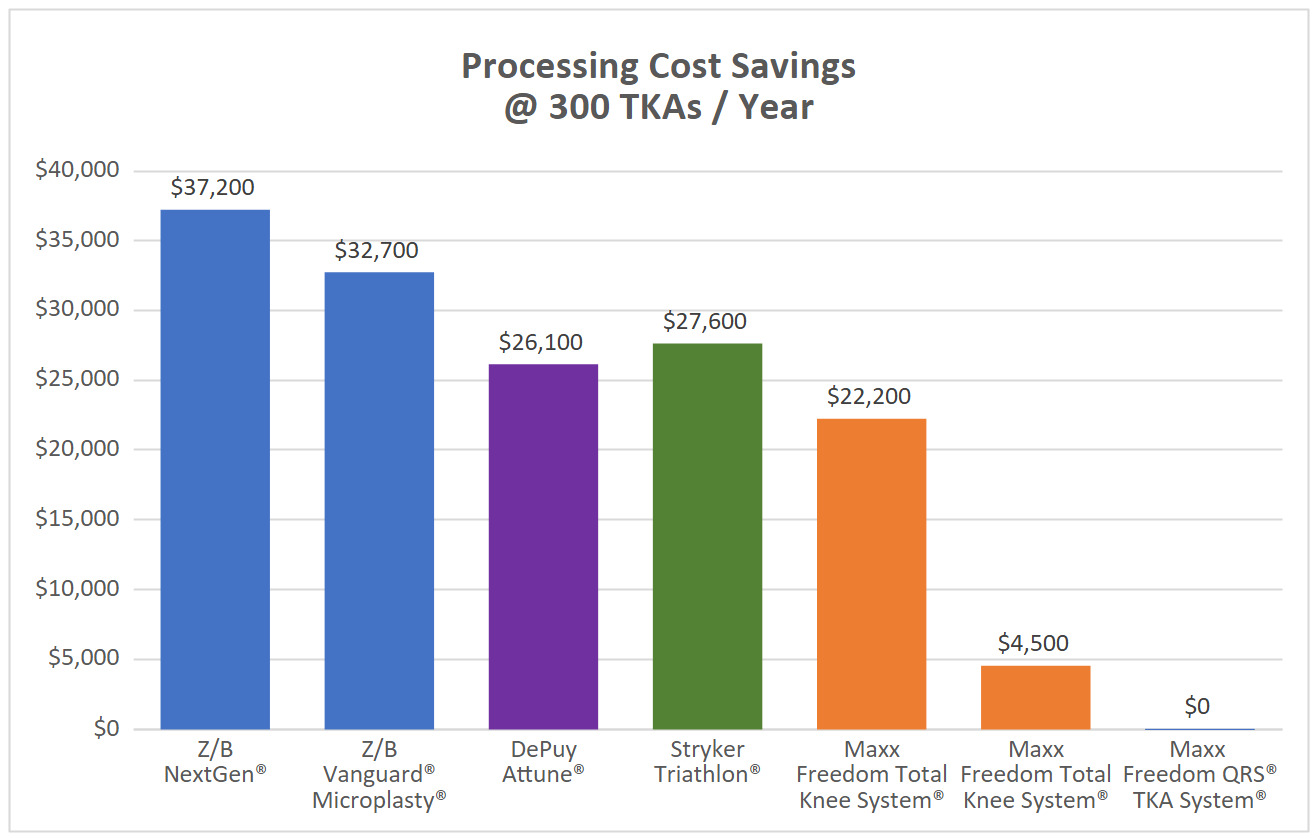

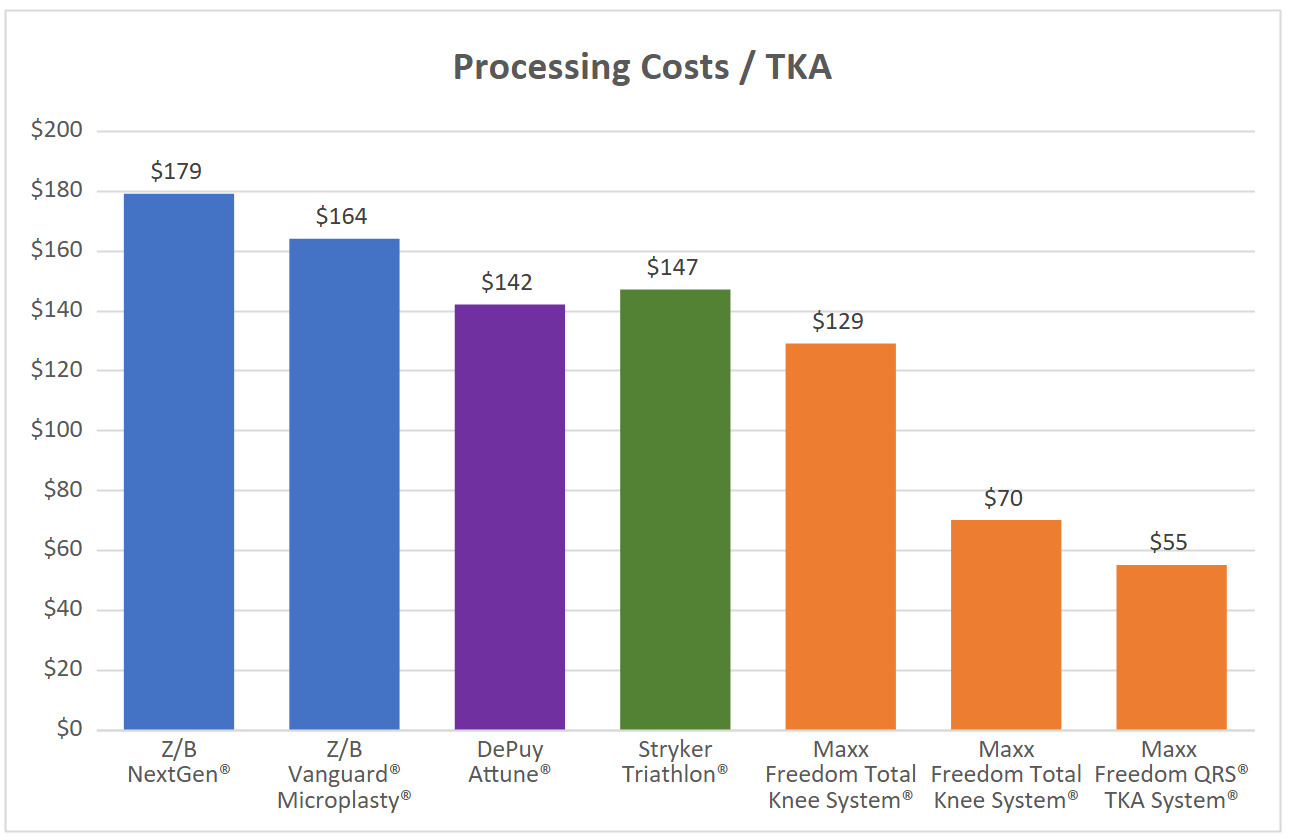

Summarized in Table 2, and Figures 1, 2, 3A-C, the Maxx Freedom Total Knee System originally utilized five (5) trays and 255 instruments, with an estimated processing cost of $130. Beginning 2019, instruments were re-organized across three (3) trays by level of constraint, yielding instrument total of 138, and an estimated central services processing cost range of $70. The subsequent instrument tray reduction strategy used in this study utilizes one (1) tray and 108 TKA instruments specific to the planned component sizing and surgeon’s instrument preferences (estimated processing cost: $55). When compared to the QRS system the reduced instrument tray processing cost per case was calculated at $55 and was considerably less than the other four ranging from $142 to $179 (Table 2, Figure 3A). Pre-operative component templating and sizing was determined, and all templated size recommendations were matched with the implanted components without any need to open additional trays for increased or decreased size dependent instrumentation.

There were no intra-operative TKA system changes or early adverse events related to the predetermined sizing and components available or used. Through 90 days All patients achieved post-operative relief of pain, restoration of function, and independent ambulation, which continued through their 1- and 2-year follow-up visits. However, there were two patients that returned for early unscheduled office / hospital visits (< 90 days): one patient presented with a superficial would dehiscence that required irrigation and debridement. The second patient reported concerns regarding delayed wound healing, was examined and placed on oral antibiotics. In both cases the “adverse events” were resolved without further issue and remained resolved through 2-year follow-up. Through two-years there were no other unscheduled office, Emergency Room, or hospital visits reported including any adverse, or severe adverse events related to the TKA in any of the study patients.

DISCUSSION / CONCLUSION

From this study we report significant estimated instrument processing cost savings when comparing standard primary TKA instrument tray configurations versus a reduced instrument tray TKA System. Matching the pre-operative component size selection with only the necessary instrumentation allowed for reduction of instrument and component inventory, without sacrificing the safe and efficacious performance of the TKA procedure within our ASC facility.

The cost-effectiveness of surgical procedures is being closely scrutinized within our national, value-based healthcare environment. Chronically overstocking instrument trays for surgery is a common practice and is historically done to avoid missing instruments during a procedure. However, the inability, or avoidance, of predicting what is really needed may be the true reason for the excessive overstocking of surgical instruments. The chronically excessive use of unnecessary and unused instrument trays adds costs including transportation, handling, set-up, tear-down, processing and storage. Across THA and TKA procedures “marginal gain” aggregates are measured for procedures, surgeon technical skills and support staff that are already highly optimized. Palsis, et al, investigated the costs for the entire episode of primary hip and knee arthroplasty using a time-driven activity-based costing (TDABC) methodology versus traditional accounting methods (Palsis et al. 2018). The breakdown of the entire surgeon-patient episode (initial clinic, through surgery and subsequent follow-up) was defined, and total costs assigned to each step. The authors showed that across the continuum of care, the surgeon-patient episodes could be investigated and specific steps in which various burdens could be identified, marginal gains strategies defined, and applied.

Reducing the TKA instrument tray burden, especially for ASCs, may influence operating room efficiency, central services turn-over and associated costs. In a matched cohort study of TKAs performed in a hospital versus ASC setting, Littleton, et al, retrospectively reviewed a matched cohort of patients undergoing primary TKA between a hospital and ASC setting. The authors reported significant time to discharge and cost reductions in the ASC over the hospital setting. The extended length of stay may be the primary contributor to total costs and may not reflect the granular costs burdens within the various areas associated with services necessary for delivery of care.

Basing component needs on pre-operative templating, component sizing was determined, the tray was built to include the templated size, plus / minus one size and including surgeon preference or formulary for TKA specific instruments. We found that all pre-operative templated size recommendations matched the same intra-operative size selected and implanted. There was no case that required a component size beyond the three sizes available in the QRS single tray. Minimizing the amount of TKA instruments and product required for each case decreases inventory handling, storage, retrieval, and re-stocking burdens of maintaining redundant instrument and product banks,

In review, we realized specific limitations of our study. First, the assumption of $0.51 cost per instrument processing was referenced from general surgical average processing costs and may not exactly represent our specific facility. Secondly, the type of facility (Hospital versus ASC) may have differing overhead processing costs and cannot be directly compared. Lastly, specific preferences for TKA specific instrument use across surgeons may differ within and across facilities, thus making the total number of instruments for the one-tray system to vary slightly. We recommend that further study of hospital and ASC instrument processing cost should include site specific accounting across the continuum of primary TKA surgical event costs (shipping, receiving, storage, retrieval, processing, sterilization, wrapping, and return to storage).

Minimizing cost burdens across the continuum of care for TKA is a continuous effort for all participants. Implementing cost efficiency without adversely affecting patient outcome is a continuous moving target. The proposed strategy has initially addressed TKA specific tray reduction through component sizing and instrumentation optimization (McLawhorn, et al. 2015). Comparative results have shown considerable processing cost reductions for the proposed instrument tray processing costs compared to various standard TKA specific instrument tray use. The effort of minimizing instrument burden through tray reduction was a feasibility requiring further study with larger numbers across various facility types is necessary and currently underway by the sponsor across multiple surgical sites. Overall, the tray and instrument reduction strategy is warranted to measure the impact on operative room efficiency burdens including room set-up, turn-over, instrument processing, and the cost per square footage of instrument tray storage.