In light of the increasing challenges facing private practice surgeons each year, it is no surprise that more and more orthopaedic groups have entered into strategic partnership transactions over the last several years, including 2024, and we expect to see even more such deals in 2025 and beyond.

This article commences with an overview of this consolidation activity and recent trends, follows with an explanation of increasing challenges facing many groups that are driving them to consider strategic partnership options, and concludes with our “Top 10” practical recommendations for orthopaedic groups when they are considering potential strategic partnership transactions.

1. Orthopaedic Consolidation: Background and Recent Trends

For the past two decades, the healthcare industry has been a hotspot of consolidation, weaving a web of mergers and acquisitions across every corner of care. It began with hospitals and other facilities, expanded to ancillary service providers like imaging centers and ambulatory surgery, and swept through the full spectrum of physician services—from primary care to specialties such as dermatology, orthopaedics, cardiology, and beyond.[1] The result? A rapidly evolving landscape reshaping how care is being delivered.

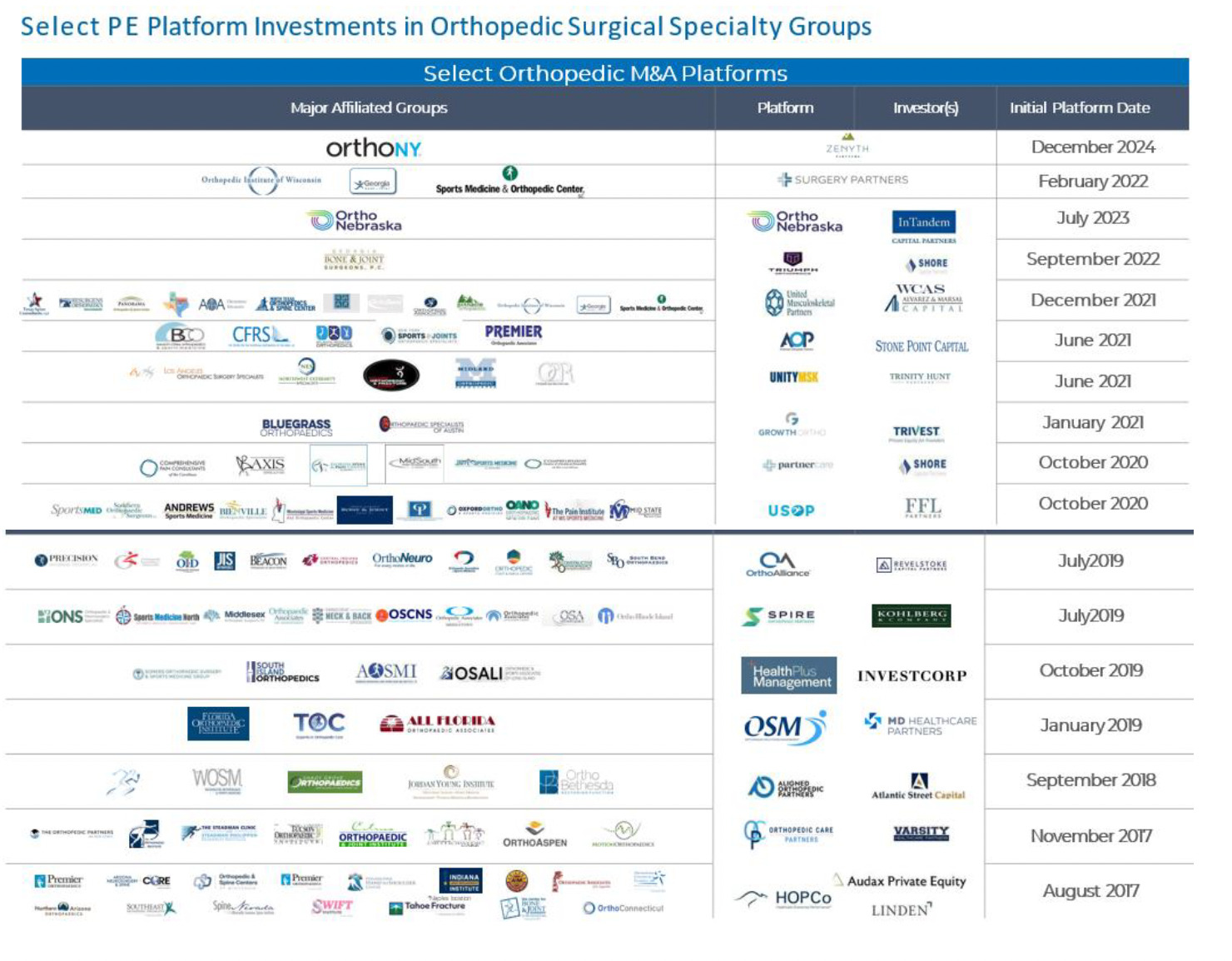

Private equity (PE) investors began partnering with orthopaedic practices in 2017 with two platforms, then five additional platforms by 2019, and after a short “pandemic break”, six more by the end of 2021, and three more over the last couple of years. As of today, there are more than 16 PE-backed management companies that are consolidating orthopaedic practices. (See Chart below).[2]

The consolidation wave in healthcare has not just been driven by traditional players—it has attracted major hospital systems and national healthcare giants like Surgery Partners and SCA Health (Optum). These organizations are actively acquiring orthopaedic practices and thereby reshaping the competitive landscape. Notably, the past year marked a significant milestone with the first major “second bite” deal in the orthopaedic sector with SCA Health’s acquisition of OrthoAlliance from Revelstoke Capital Partners. This move signals a new chapter in the industry’s ongoing transformation.

A “second bite” or “exit” transaction for a PE platform is when a larger company or investor purchases the platform, which involves the private equity fund’s investors receiving the return of their invested capital (with appreciation), as do physicians who are holding rollover equity in the platform provided in connection with joining the platform via their partnership transaction.[3]

Further, we expect that other PE-backed orthopaedic platforms are likely to enter into “second bite” transactions during 2025 because PE investors expect the return of their capital, on average within 5 years, and some platforms that have far surpassed this timeframe have not yet provided returns to their investors. Several orthopaedic platforms were in the market to exit over the last couple of years, but post-pandemic caution caused delays. Further, 2024 was a slow year overall for healthcare transactions due to a combination of macro-economic conditions (e.g., high interest rates, heightened antitrust scrutiny, etc.) as well as hesitancy in advance of the 2024 presidential election.[4]

Now that interest rates are declining, and Republicans control the White House and Congress, robust consolidation activity in the healthcare industry will resume during 2025 and thereafter, including some second bite transactions.

2. Why So Many Orthopaedic Groups Are Entering Strategic Partnership Transactions

Transaction activity involving private orthopaedic practices nationwide is being driven primarily by the escalating challenges they are facing each year, including:

a. Year after year reductions in reimbursement for physician services from Medicare, with many commercial payors following suit.[5]

b. Substantial increases in the costs of operating a medical practice – including:

i. Staff salaries at all levels – PAs/NPs, nurses, medical assistants, imaging technicians, receptionists, billers/coders, etc.

ii. Medical supplies and equipment

iii. Health insurance for employees

iv. Malpractice insurance for clinicians

The combination of items a. & b. above has resulted in year over year reductions in the take home compensation of many surgeons across the country.[6]

c. Power players in the local market – such as hospital systems, Optum, and others – acquiring primary care physicians (referral sources), and directing them to refer to their fellow employed orthopaedic surgeons. [7]

d. Consolidation elsewhere in the local market (including by other orthopaedic groups) resulting in larger, more well-capitalized competitors.[8]

e. A slow but continuous transition to value-based care programs and direct contracting with self-insured employers, which requires advance data analytics and IT systems, and care coordination staff – all at great expense – in order to succeed.[9]

f. Acceleration in the transition to providing advanced care in the outpatient setting, requiring investment of capital in high-end ASCs, imaging, etc. [10]

Due to these increasingly strong headwinds, many groups are at least exploring various potential strategic options – including various pros and cons of each – with the hope of better positioning their groups for future success.

Larger, well-capitalized organizations with seasoned healthcare executives can help to mitigate these challenges and improve a practice’s financial results, as further described below:

Facing a host of these challenges, many orthopaedic groups are evaluating strategic partnerships to determine their suitability and “cultural fit”.

Nevertheless, despite mounting pressures and challenges, some practices have chosen to “stay the course” with the goal of remaining true to their values and vision without joining forces with larger organizations. For those groups, however, it is imperative to implement a comprehensive, self-funded plan to counteract these obstacles and sustain or enhance financial performance annually.

Effective fiscal management is crucial for independent practices to thrive. This includes prudent budgeting, resource allocation, and investment strategies tailored to the unique needs of orthopaedic practices. By utilizing data-driven insights, practices can identify areas for improvement and implement strategies to enhance their financial performance.

Additionally, addressing recruitment challenges is essential. Implementing innovative recruitment strategies, such as leveraging technology and offering competitive benefits, can help attract and retain skilled clinicians. Building a positive workplace culture and providing opportunities for professional development are also key factors in retaining talent.

By focusing on these areas, independent orthopaedic groups may be able to navigate the complexities of the healthcare landscape and achieve long-term success on their own.

3. Financial Benefits & Wealth Planning Strategy

There are also financial benefits to certain partnership transactions, including monetization and “personal wealth diversification”. As the healthcare marketplace continues to change and there is increasing uncertainty regarding what the healthcare industry will look like in the long-term, there is bona fide risk that the value of orthopaedic practices could decline in the future.

Recognizing your medical practice as a valuable business asset is a crucial starting point, as it constitutes a significant portion of your personal wealth portfolio. Wealth advisors often caution against over-concentration in a single asset category, especially those with increasing risk or uncertainty. Diversifying your investment portfolio can help mitigate potential risks and enhance financial stability.

By entering into a partnership transaction, especially at a time when market valuations are “healthy”, you benefit from monetizing the value of your ownership interest, the cash portion of which can then be invested in a different class of assets that may be in a more desirable, high-growth sector with less future uncertainty (such as AI or other cutting-edge industries).

Further, in most cases, the cash proceeds received by physicians in such a transaction will be “tax-efficient”, meaning they would be subject to more favorable long-term capital gains tax rates (entailing 18-20% less taxes).

Sale transactions involving hospitals or national companies are more likely to involve “all cash” purchases, although some of these “buyers” have been open to including physicians in post-closing ownership of the local venture/entity.

Partnerships with PE-backed platforms, however, routinely entail 60-70% of the practice’s value being paid in cash at closing (to be invested as described above), with the balance of 30-40% of the value constituting rollover equity in the PE platform. This is the standard model for private equity investors because it very closely aligns the physicians with the goals and objectives of the platform, and rewards the physicians (proportionally to PE investors) for the growth and success of the platform in the future.

Although not every PE platform achieves its investment objective of at least tripling its invested capital, many are successful, and when the PE investors “exit” their investment (in what is also called a “second bite” transaction),[11] the physicians enjoy the same enhanced share value on their rollover equity (assuming it is the same “class” of equity), most of which is subject to more favorable/efficient tax rates described above.

4. Top 10 Practical Recommendations for Orthopaedic Groups

As discussed above, a strategic transaction is not right for every group. But the following are practical recommendations for all orthopaedic groups to consider, in light of the increasing challenges they are facing, and the robust consolidation activity they are seeing throughout the country.

-

Make an Informed Decision. Some orthopaedic surgeons have a negative knee-jerk reaction to any kind of transaction, private equity or otherwise. But, before making a fully informed decision about what (if anything) is right for your group, learn comprehensive details about different potential strategic options, and the pros and cons of each.

-

Culture Trumps Everything. Regardless of the numbers being offered by a potential partner, make sure that you are very comfortable with the “culture” of the potential partner – a hospital, PE platform, national company, or otherwise – such as:

a. Do you trust them as good people/individuals?

b. Are you convinced they are very experienced and are likely to execute on their plan to improve your practice?

c. Are you “on board” with their philosophy and business plan?

-

Confidence in “Income Repair”. Income repair is the concept that you, as surgeons, will do better compensation-wise after you enter into a partnership transaction. This is most important if joining a PE platform, because PE transactions involve an initial “compensation reduction” (aka “scrape”), and physicians should have comfort that the benefits of the platform are “real” and will result in your compensation being “repaired” over a few years to the same amount, or even higher, than before the partnership transaction.

Thus, before committing to a particular partner, obtain details demonstrating their ability to provide (and their past record of success in providing) significant “income repair” – such as via:a. enhanced payor rates;

b. commencing or expanding ancillary services (e.g., ASC, imaging, therapy, orthopaedic urgent care, etc.);

c. commencing or expanding participation in value-based care programs;

d. economies of scale through the use of centralized services (e.g., billing, human resources, managed care contracting, compliance, IT services, call centers, etc.); and

e. savings via group purchasing (e.g., reduced cost of equipment & supplies, reduced malpractice insurance premiums, reduced health plan cost for staff, etc.).

-

Solid (Proven) Plan for Recruiting New Physicians. You should also be convinced that your partner has a solid plan for recruiting new physicians to the group in the future who can become partners in the normal course on reasonable terms. If a particular platform has been operating for several years, then ask for details regarding their track record of successfully doing so!

-

Assess the Extent of the Partner’s Leverage (Debt). Your financial advisor should conduct an analysis of whether your potential partner is “over-leveraged” (i.e., has too much debt and/or on bad terms). Companies that are overleveraged will face more challenges in achieving their objectives for growth and success.

-

“Doc-to-Doc” Diligence. Before finalizing your selection of a potential partner for a strategic partnership, speak with other doctors who have partnered with that platform to help you assess, as objectively as possible, each of the topics in Items 4-5 above. For an orthopaedic platform that has been around for a few years, this means calling junior and mid-level surgeons at practices that previously joined the company to assess “off the record” (and confidentially) whether they are happy at the company, and whether the platform has lived up to its commitments.

In addition, if you are considering a PE platform, also ask your advisors to identify other physician specialties that such PE firm has previously invested in – as many PE firms investing in orthopaedics also have experience in other physician specialties, such as eyecare, dermatology, urology, OBGYN, etc. If so, then call some of the junior and mid-level physicians there and ask the same questions.

In both cases, however, do not just call physicians on a list of references that is provided by the PE platform, as most of them likely were leaders of groups that previously transacted, or are currently in some kind of managerial role at the company. -

Get Your Practice’s House in Order Prior to Exploring Options. We wish every group spent a few months (and a very small amount money) in getting ready for a transaction before exploring potential strategic options. Doing so truly helps to maximize the value of your practice – and conversely, avoids devaluation. This entails several components:

a. Confirm there is wide consensus among the owners of the practice to explore potential strategic options, and to move forward if a “good” partner is identified and the terms are “right”.

b. Also get consensus among the practice’s owners as to how proceeds of a transaction should be split – and whether the practice’s governing documents and tax status allow for such or require modification.

c. Assess with legal and tax counsel the group’s corporate and tax structure to determine if there would be advantages to a restructuring long before starting to explore options (e.g., in a prior tax year), especially in light of how the group desires to split proceeds.

d. Have legal counsel walk you through a checklist of basic regulatory compliance matters, and also financial housekeeping matters, to see if certain “easy fixes” can be quickly implemented– all which can ensure a higher practice value, as well as a smoother transaction process if you decide to move forward with a deal.

-

Get Your Practice’s Real Estate in Order in Advance. If you own one or more parcels of real estate which your practice uses, we cannot stress enough how important it is to assess your “related party” lease, to make sure that it is an “arms-length” commercial lease, with triple net terms and market rental amounts that reasonably escalate each year, and has a term of 10-15 years.

If such a lease is not in place, it should be put in place ASAP. This will help to maximize the value of your real estate in the event that you decide to sell it at some point after entering into a partnership transaction. -

Personal Wealth Planning in Advance of a Major Transaction. You should also schedule a meeting with your accountant and personal wealth advisor long before you decide to pursue a strategic transaction, as they may have very useful advance planning ideas to maximize the overall benefit and impact of your transaction proceeds.

-

Engage Experienced Professional Advisors. Engage professional advisors – investment bankers, attorneys and accountants – who have substantial experience advising medical groups on strategic partnership transactions (20 or more deals). In this regard:

a. Interview at least 2-3 experienced investment bankers before deciding which one seems like the best fit for your group. (And the same for attorneys and accountants).

b. Most importantly, before signing an LOI (letter of intent), first have it reviewed by a healthcare transactions attorney with substantial experience. If people tell you its “non-binding”, do not listen, as the signed LOI will be referred back to later in the deal negotiations (as if it is the “constitution of the deal”). Thus, a legal review is very important – both in regard to the terms included in the draft LOI that is provided to you, and also with respect to other terms that are important to you and should also be included.

In conclusion, by considering the various factors described in this article, and the above recommendations, orthopaedic groups can make informed decisions about pursuing strategic partnerships or staying independent – in both cases, with the goal of positioning themselves for sustained success and profitability in the future amid ongoing transformation and increasing challenges throughout the healthcare industry.

Zachary Levinson, Jamie Godwin, Scott Hulver & Tricia Neuman, Ten Things to Know About Consolidation in Health Care Provider Markets, KFF (Apr. 19, 2024), https://www.kff.org/health-costs/issue-brief/ten-things-to-know-about-consolidation-in-health-care-provider-markets/#; Meg Bryant, Surgery Centers Seeing Lots of Consolidation, Healthcare Dive (Mar. 24, 2017), https://www.healthcaredive.com/news/surgery-centers-seeing-lots-of-consolidation/438838/; Cheryl Proval, The 20 Largest Outpatient-Imaging Center Chains: Consolidation Continues, Hospital Alignment Takes Root, Radiology Bus. (Aug. 18, 2015), https://radiologybusiness.com/topics/medical-practice-management/20-largest-outpatient-imaging-center-chains-consolidation.

A comparison of this current chart against a similar chart in a 2020 JOEI article reveals just how active investors and orthopaedic groups have been over the last four years. See Gary Herschman & Hector Torres, Private Equity Partnerships in Orthopedic Groups: Current State and Key Considerations, 1 J. Orthopaedic Experience & Innovation 1 (2020), https://journaloei.scholasticahq.com/article/17721-private-equity-partnerships-in-orthopedic-groups-current-state-and-key-considerations.

For details on the financial aspects of second bite transactions, see footnote 11 below.

Sabrina Valle, Healthcare Dealmakers Eye M&A Resurgence in Second Trump Term, Reuters (Jan. 13, 2025), https://www.reuters.com/markets/deals/healthcare-dealmakers-eye-ma-resurgence-second-trump-term-2025-01-13/.

Bruce A. Scott, M.D. (AMA President), Congressional Action on Medicare Payments Must Occur this Year, Am. Med. Ass’n (Dec. 2, 2024), https://www.ama-assn.org/about/leadership/congressional-action-medicare-payments-must-occur-year.

Med. Grp. Mgmt. Ass’n Staff Members, Nearly All Medical Groups Still Feeling the Squeeze of Rising Operating Expenses, Med. Grp. Mgmt. Ass’n (June 26, 2024), https://www.mgma.com/mgma-stat/nearly-all-medical-groups-still-feeling-the-squeeze-of-rising-operating-expenses.

Stan Schwartz, The Modern-Day Twisted Ethics of Physician Referrals, MedCity News (July 15, 2019), https://medcitynews.com/2019/07/the-modern-day-twisted-ethics-of-physician-referrals/; see also Reed Abelson, Corporate Giants Buy Up Primary Care Practices at Rapid Pace, N.Y. Times (May 1, 2023), https://www.nytimes.com/2023/05/08/health/primary-care-doctors-consolidation.html.

See Chart of Orthopaedic PE platforms above, and footnote 2 above.

Matthew Hellinger & Ian Goldberger, The State of Value-Based Care, Med. Econ. (June 21, 2024), https://www.medicaleconomics.com/view/the-state-of-value-based-care.

Alexandra Schumm, As More Inpatient Care Shifts to Outpatient Settings, Competition in Ambulatory Surgery Intensifies, Chartis (June 28, 2024), https://www.chartis.com/insights/more-inpatient-care-shifts-outpatient-settings-competition-ambulatory-surgery-intensifies.

In second bite transactions, physicians who are still actively practicing usually have the option to sell around 50% (+/-) of their equity, taking more “chips off the table” (cash) to invest elsewhere, and continue to own the balance of their rollover equity – which likely will increase in value in the future when the new investor deploys additional capital to further grow and expand the platform. Physicians who are on the verge of retiring soon may be able to sell all of their rollover equity in a second bite transaction.

For a short webcast containing more details on “second bite transactions” see Epstein Becker Green, How Do “Second Bite” Transactions Work for Physicians in Private Equity Partnerships?, Epstein Becker Green: Docs Doing Deals (2023), https://www.ebglaw.com/insights/events/how-do-second-bite-transactions-work-for-physicians-in-private-equity-partnerships-on-demand-webcast.